TL;DR:

- Many retail traders mistakenly believe savings alone ensure financial security, but risk management and protections are essential. True financial security allows traders to withstand shocks, sustain losses, and achieve goals without panic; it requires buffers, diversification, insurance, and disciplined risk controls. Building a resilient financial system, regularly reviewing it, and applying consistent strategies are crucial for long-term stability in active trading.

Most retail traders assume that stashing away a percentage of their income each month is enough to call themselves financially secure. It’s not. Saving money is one piece of a much larger puzzle, and for traders and investors who actively expose capital to market volatility, the gap between “having savings” and “being financially secure” can be enormous. This guide breaks down what genuine financial security looks like for active market participants, presents actionable frameworks for building it from the ground up, and challenges some of the most persistent myths standing between you and real financial stability.

Table of Contents

- What is financial security and why does it matter?

- Building your financial foundation: Emergency fund, debt, and insurance

- Diversifying your portfolio: Comparing allocation strategies

- Beyond numbers: Holistic financial planning for traders and investors

- Our perspective: The uncomfortable truth about financial security for active traders

- Take the next step toward financial security with Olla Trade

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Savings aren’t enough | True financial security requires risk management, insurance, and strategic planning—beyond just saving money. |

| Diversification matters | Spreading investments across asset classes lowers risk and supports long-term financial stability. |

| Build your foundation | Establish an emergency fund, manage debt, and secure relevant insurance before taking trading risks. |

| Adopt holistic planning | Integrating purpose and resilience ensures your financial strategy is robust and adaptable. |

| Regular strategy review | Review your portfolio strategies annually or after major life events to maintain alignment with your goals. |

What is financial security and why does it matter?

Financial security is not a number in your bank account. For retail traders and investors, it’s a state where your financial life can absorb shocks, sustain losses, and still support your goals without forcing you into panic decisions.

Savings alone are insufficient without proper risk management and insurance in place. This is a fundamental distinction that separates experienced investors from those who are simply lucky. A trader with $50,000 in savings but no health insurance, no emergency buffer, and a single concentrated position is far more vulnerable than a trader with $20,000 spread intelligently across assets with proper protections in place.

The concept of clarity over certainty matters here. You will never have certainty in markets. What you can have is clarity about your risk tolerance, your income needs, and your protection layers. That clarity is what allows confident decision-making even during volatility.

Here’s what financial security actually requires for retail traders and investors:

- Emergency fund: A liquid cash buffer to cover living expenses without touching investments

- Diversified portfolio: Assets spread across different instruments and markets

- Risk management systems: Stop-losses, position sizing, and exposure limits

- Insurance coverage: Protection against medical, disability, or income disruption events

- Debt control: No high-interest liabilities that can drain capital during drawdowns

- Understanding investment regulations: Knowing the legal framework within which your assets operate

One nuance worth addressing: concentrated portfolios are not automatically reckless. Research shows that experienced analysts with deep research capabilities can manage portfolios of around 25 stocks effectively. Women retail investors, in particular, often display higher concentration tendencies that can work well when backed by diligent research. The key is knowing your analytical edge.

“Financial security isn’t the absence of risk. It’s the presence of a system that protects you when risk becomes reality.”

Understanding the emergency fund importance is one of the first steps to building that system correctly.

Building your financial foundation: Emergency fund, debt, and insurance

With financial security defined, let’s explore the foundational protections every investor should build first. Before you optimize returns or research the next trade, these fundamentals need to be in place.

According to FINRA’s guidance for 2026 investors, the key mechanics of financial security include building an emergency fund covering 3 to 6 months of expenses, active debt management, maintaining a diversified portfolio, and carrying insurance against major risks such as medical emergencies. These are not optional extras. They are structural pillars.

How to calculate your emergency fund size

Use this simple framework to size your emergency fund accurately:

| Factor | Conservative traders | Active/aggressive traders |

|---|---|---|

| Monthly fixed expenses | 3x coverage | 6x coverage |

| Income source diversity | Single income: 6 months | Multiple streams: 3 months |

| Market exposure level | Low leverage: 3 months | High leverage: 6+ months |

| Health insurance status | Insured: 3 months | Uninsured: 6+ months |

The more volatile your trading strategy, the larger your emergency fund should be. A forex scalper running high leverage needs more buffer than a long-term ETF investor.

Building the foundation step by step

- Audit your monthly expenses. Track fixed costs (rent, utilities, subscriptions) and variable costs (food, transport, trading fees) separately.

- Open a dedicated high-yield savings account. Keep this completely separate from your trading capital. It is not for trading. Ever.

- Target your emergency fund first. Before putting extra capital into markets, fully fund your emergency buffer.

- Tackle high-interest debt next. Credit card debt above 10% interest annually is an investment killer. Eliminate it aggressively.

- Review your insurance coverage. Health, disability, and income protection policies should be in place before you scale your trading activity.

Pro Tip: Keep your emergency fund in a liquid, accessible account, not in money market funds or bonds that take time to liquidate. When emergencies happen, you need cash immediately, not in three business days.

Good practices for managing trading risk will reinforce your overall financial foundation, since traders who manage risk well in markets tend to apply the same discipline to personal finances.

Also explore this detailed emergency fund guide for step-by-step advice tailored to individual financial situations.

Diversifying your portfolio: Comparing allocation strategies

Once your foundation is secure, it’s time to tackle the heart of financial security: diversification. The way you spread your capital across assets can dramatically affect both your returns and your peace of mind.

There are three main frameworks that sophisticated retail traders and investors use, each with distinct risk/return profiles.

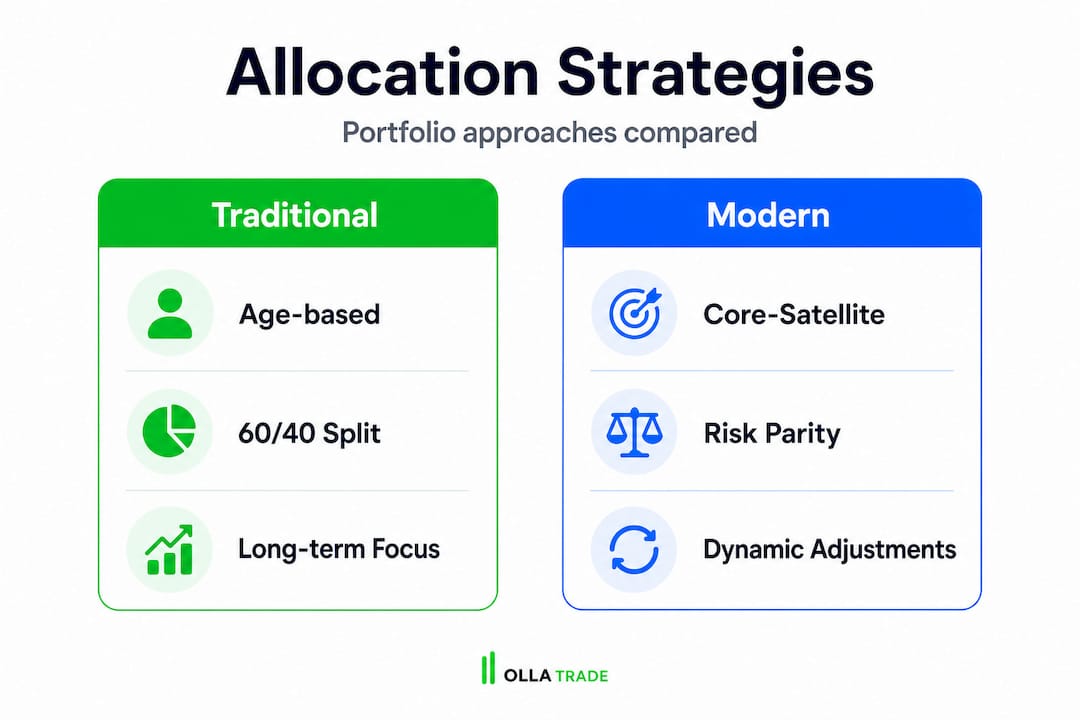

1. Traditional age-based allocation

This is the original framework. In your 20s and 30s, you hold 80 to 90% in equities and a small portion in bonds. By your 40s and 50s, you shift to 60 to 75% equities. By retirement, bonds and safer assets dominate. It’s simple and has worked historically, but it ignores individual risk profiles entirely.

2. Core-satellite strategy

Here, 60 to 80% of your portfolio is anchored in broad index funds (like VTI or S&P 500 trackers), while 20 to 40% is allocated to targeted, higher-conviction positions in sectors, themes, or individual stocks. This approach preserves stability while allowing for active selection. Research on diversified portfolio construction confirms this hybrid model as a strong middle ground for modern investors.

3. Risk parity

Rather than allocating by dollar amount, risk parity allocates by risk contribution. Stocks get 25 to 35% (they’re volatile, so they still dominate risk), bonds take 40 to 50%, and commodities fill 15 to 20%. Every asset class contributes roughly equal risk to the portfolio. The result is smoother performance across market cycles, though returns can lag pure equity portfolios in strong bull markets.

| Strategy | Equity % | Bond % | Other | Best for |

|---|---|---|---|---|

| Traditional (age-based) | 60 to 90% | 10 to 40% | Minimal | Long-term, passive investors |

| Core-satellite | 60 to 80% broad index | 0 to 20% | 20 to 40% targeted | Active stock pickers |

| Risk parity | 25 to 35% | 40 to 50% | 15 to 20% commodities | Volatility-averse traders |

Pros and cons of each approach:

- Traditional: Simple and proven, but ignores volatility tolerance and current market dynamics

- Core-satellite: Flexible and adaptable, but requires active research for the satellite portion

- Risk parity: Excellent for downside protection, but complex to rebalance and may underperform in long bull runs

Understanding how portfolio indices support diversification is essential when selecting your core positions. And if you’re considering adding real assets, explore why trading commodities can serve as both a hedge and a return driver within a diversified structure.

For additional frameworks, read this guide on diversifying investments naturally and this breakdown of asset allocation strategies for 2026.

Beyond numbers: Holistic financial planning for traders and investors

You’ve explored allocation strategies. Now discover how to integrate mindset and adaptability for long-term financial well-being, because numbers alone won’t get you there.

There are two broad camps in financial planning. The traditional, numbers-based view says security comes from steady income, a diversified portfolio, and hitting specific benchmarks. The holistic view says security comes from clarity, resilience, and purpose. Both views contain truth, and active traders need both.

Here’s what the numbers actually tell us: retail investors hold approximately 71% equities in their portfolios, based on 2016 data that still reflects current behavior patterns. Stock ownership across U.S. households now sits at roughly 74% in 2025. High concentration is extremely common among retail investors, which means most people are taking on more individual-stock risk than they realize.

But the emotional and psychological dimension matters just as much. Traders who feel financially secure are measurably better decision-makers. When you’re not worried about losing your emergency fund or facing debt collection, you can trade from a position of strength rather than desperation. That’s not soft advice. It directly impacts your P&L.

“The goal of financial planning is not to predict the future. It’s to build a structure that can handle whatever future arrives.”

Holistic planning means:

- Setting clear, written financial goals for the short and long term

- Scheduling quarterly reviews of your portfolio, debt, and insurance coverage

- Tracking your emotional responses to market events as data, not as noise

- Aligning your investment strategy with your actual life goals, not just abstract return targets

Pro Tip: Short-term goals (fund the emergency account, pay off credit cards) and long-term goals (build retirement wealth, achieve trading income) need separate mental frameworks. Conflating them leads to using emergency funds for trading opportunities, which is a pattern that destroys financial security faster than any market crash.

Developing a clear investment strategy for your future and reviewing it consistently is the practical application of this holistic approach. You can also strengthen your trading decision-making by studying 12 essential trading strategies that successful retail traders actually apply.

Our perspective: The uncomfortable truth about financial security for active traders

Here is the candid version that most financial guides skip: the popular “save and diversify” formula is necessary but not sufficient. We’ve seen traders with well-diversified portfolios, strong historical returns, and consistent monthly savings get completely derailed by a single unexpected medical expense, a job loss that dried up their trading capital, or a margin call they couldn’t cover because their emergency fund was in the same brokerage account as their active trades.

The formula breaks down when people treat financial security as a portfolio optimization problem rather than a life management problem. Diversification protects you from market risk. It does nothing to protect you from income disruption, health crises, or behavioral mistakes made under financial stress.

The hard-won lesson from retail trading is this: the traders who survive long enough to become consistently profitable are not always the smartest analysts. They are the ones who built protective structures around their trading activity. They separated their living expenses from their risk capital. They carried insurance. They reviewed their exposure regularly. They made boring, disciplined decisions during calm periods so that volatile periods didn’t force their hand.

Overconfidence is the specific pitfall we see most often. A few strong months of returns can create the illusion that the savings and insurance pieces are unnecessary luxuries. They are not. Markets can move against you faster than your analytical edge can protect you, and the cost of being wrong without a safety net is measured in years of rebuilding, not just dollars lost.

We also see traders ignore how index exposure shapes their overall risk when they’re already running concentrated individual positions. The interaction between your equity portfolio and the broader market matters more than most retail traders account for.

The practical wisdom here is simple: take ownership of your financial security as a complete system. Review it at least once a quarter. Adjust your insurance as your income and exposure change. Keep your emergency fund untouchable. Apply the same rigor to your personal financial structure that you apply to your trading setups.

Take the next step toward financial security with Olla Trade

Understanding the frameworks is only half the job. Applying them through reliable tools and platforms is where it becomes real for your financial life.

At Olla Trade, we’ve built a platform designed to support retail traders at every stage of their financial journey, from learning the fundamentals to executing sophisticated strategies across forex, CFDs, metals, indices, and cryptocurrencies. Whether you’re building your first diversified portfolio or refining your forex trading approach with advanced tools, the resources are here. Explore our curated top trading tools to identify the instruments that fit your strategy, or follow our step-by-step forex trading guide to start managing risk from day one. Financial security is built through consistent, informed action.

Frequently asked questions

How much should I set aside for an emergency fund as a trader?

Most experts recommend 3 to 6 months of expenses as your emergency fund baseline, with the higher end applying to traders who use leverage or run concentrated positions.

Is diversification still necessary if I’m an experienced stock picker?

Diversification still matters as a risk management layer, but concentrated portfolios of roughly 25 stocks can work well for investors who conduct thorough, disciplined research on every position.

What are the most common mistakes that undermine financial security?

Skipping the emergency fund, ignoring insurance coverage, and overconcentrating capital in a single asset class are the most frequent structural errors that retail traders make.

How do risk parity strategies smooth returns compared to traditional 60/40 allocation?

Risk parity distributes risk equally across asset classes rather than allocating by dollar value, which produces lower drawdowns and more consistent returns across different market environments than the classic 60/40 stock/bond split.

How often should I review my asset allocation strategies?

Review your asset allocation at least once per year, and immediately after any significant life event such as a change in income, major expense, or significant shift in your market exposure.