要約:

- Order execution involves the entire process of receiving, routing, matching, and confirming trades, with each stage affecting your final price. Choosing the right order type and understanding technological factors like latency and routing are essential for optimizing trade quality and minimizing costs such as slippage. Proper knowledge of execution mechanics enables traders to make informed decisions, improve consistency, and manage trading expenses effectively.

Order execution is defined as the complete process by which a buy or sell order is received, validated, routed, matched, and confirmed in a financial market. Every trade you place, whether on forex pairs, CFDs, or equities, depends entirely on this process working correctly. Modern electronic exchanges complete this sequence in milliseconds to microseconds, meaning the gap between your click and your fill is measured in fractions of a second. Understanding what is order execution, and how each stage affects your final price, is the difference between trading blind and trading with a real edge.

What is order execution and how does it work step by step?

Order execution, also called trade execution, follows a precise sequence from the moment you submit an order to the moment your broker confirms the fill. Each stage introduces variables that affect your final price and certainty of execution.

Here is how the order execution process unfolds:

- Order submission. You place a buy or sell order through your trading platform. The platform sends this to your broker’s Order Management System (OMS), which logs the order, timestamps it, and prepares it for processing.

- Validation and compliance checks. The OMS verifies your account balance, margin availability, and whether the order meets regulatory requirements. Orders that fail these checks are rejected before they ever reach the market.

- Smart Order Routing. Once validated, a Smart Order Router (SOR) analyzes available execution venues, including exchanges, Electronic Communication Networks (ECNs), and wholesale market makers. Smart Order Routers analyze multiple venues for liquidity, price improvement, and fees simultaneously to select the optimal path.

- Matching engine. At the chosen venue, a matching engine pairs your order with a counterpart. Electronic exchanges use matching engines and order books to pair buy and sell orders based on price-time priority in micro- to nanoseconds.

- Execution reporting. Once matched, the venue sends a fill report back through the chain to your broker and then to your platform. You see the confirmation, including fill price and quantity.

- Settlement. Execution and settlement are not the same event. Since May 2024, the standard settlement cycle for U.S. equities is T+1, meaning the legal transfer of shares and cash completes one business day after the trade date. Execution happens in milliseconds; settlement takes a full business day.

プロのヒント: Always check your broker’s execution policy, not just their advertised speed. Ollatrade publishes its 注文執行ポリシー so you can see exactly how orders are routed and prioritized before you trade.

What are the types of order execution and their trade-offs?

Choosing the right order type is one of the most direct ways you control execution quality. Each type makes a different trade-off between speed, price certainty, and the probability of getting filled at all.

| Order type | スピード | Price control | Fill certainty |

|---|---|---|---|

| Market order | すぐに | なし | 非常に高い |

| Limit order | Delayed or never | 満杯 | Conditional |

| 停止命令 | Triggered | None after trigger | High after trigger |

| Stop-limit order | Triggered | Full after trigger | Conditional |

| Fill or Kill (FOK) | すぐに | 満杯 | All-or-nothing |

| Immediate or Cancel (IOC) | すぐに | 満杯 | Partial fill possible |

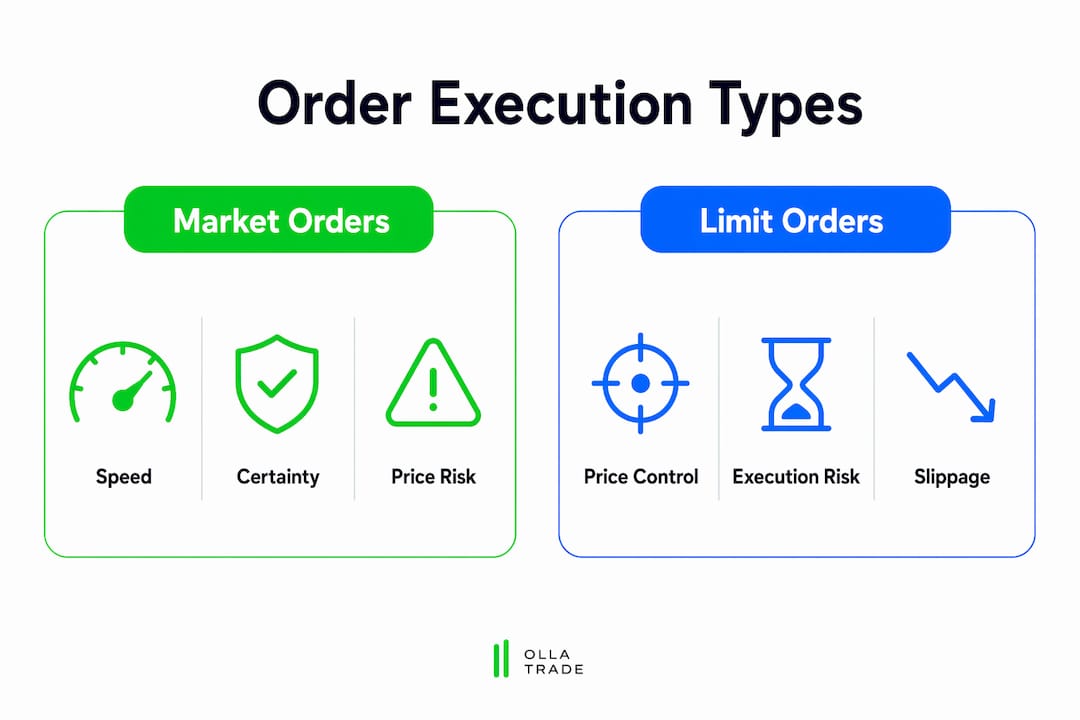

Market orders prioritize speed and certainty of execution but surrender price control entirely. In a fast-moving forex market, a market order on a major pair like EUR/USD fills almost instantly, but during a news spike, the fill price can differ significantly from what you saw on screen.

Limit orders give you full price control but introduce execution risk. If the market never reaches your specified price, the order simply does not fill. Professional traders use limit orders as their default in liquid markets precisely because they eliminate the cost of immediacy.

Stop and stop-limit orders automate risk management. A stop order converts to a market order when a trigger price is hit, which guarantees a fill but not a price. A stop-limit order converts to a limit order at the trigger, which protects price but risks no fill if the market gaps through your level.

Advanced conditional orders like Fill or Kill and Immediate or Cancel are tools used primarily by institutional desks. FOK requires the entire order to fill at once or be canceled. IOC accepts partial fills and cancels the remainder. Both are designed to prevent partial fills from creating unintended exposure.

Professional traders split large orders into smaller tranches to minimize market impact, a practice that separates institutional execution from typical retail methods. A single large market order in a thinly traded instrument can walk the order book and fill at progressively worse prices.

プロのヒント: In volatile markets, avoid market orders on instruments with wide spreads. Use limit orders with a small buffer above or below the current price to capture fills without paying the full cost of immediacy.

How slippage, spreads, and latency affect execution quality

Execution quality is not binary. It exists on a spectrum, and three factors determine where your fills land on that spectrum: the bid-ask spread, slippage, and latency.

The bid-ask spread is the static cost of immediacy. Every time you execute a market order, you pay the spread by buying at the ask and selling at the bid. On liquid pairs like EUR/USD, this cost is minimal. On exotic currency pairs or thinly traded CFDs, the spread alone can represent a meaningful percentage of your expected profit.

Slippage is the dynamic cost that arises when your actual fill price differs from your expected price. It is most common in retail market orders during high volatility, wide spreads, or when large orders consume multiple levels of the order book. Slippage is not a broker failure. It reflects the reality of supply and demand at the exact moment your order arrives at the venue.

Key factors that drive slippage:

- Market volatility. News events, central bank announcements, and economic data releases cause rapid price movement between order submission and fill.

- Order size relative to liquidity. Large orders that exceed liquidity at the best price walk the order book, filling at progressively worse prices.

- Instrument liquidity. Major forex pairs have deep order books and minimal slippage. Micro-cap stocks or low-volume crypto pairs have shallow books and high slippage risk.

- Time of day. Liquidity thins during off-hours and around market open and close, increasing slippage probability.

Latency is the time delay between your order submission and its arrival at the execution venue. Latency in execution arises from routing path, validation, Smart Order Routing, message volume, and order complexity, not just your internet connection. A broker with a slow OMS or a congested SOR introduces latency that can cost you price improvement, especially in fast markets.

Price improvement occurs when trades execute at better prices than the National Best Bid and Offer (NBBO), mostly provided by wholesale market makers routing retail orders. It is a measurable benefit but not guaranteed, and it depends heavily on your broker’s routing agreements. You can review Ollatrade’s execution information to understand how fills are reported and what price improvement looks like in practice.

For a deeper look at how real trading costs affect your bottom line, Ollatrade’s guide on slippage and retail costs breaks down what you are actually paying per trade.

How OMS, EMS, and Smart Order Routers shape your execution

The technology stack behind order execution is invisible to most traders, but it directly determines the speed, cost, and reliability of every fill you receive.

Order Management Systems track the multi-day order lifecycle for compliance and settlement, while Execution Management Systems focus on hyper-optimized, real-time order routing and execution. In practical terms, the OMS is the record-keeper and the EMS is the speed engine. Professional trading desks run both. Retail brokers typically integrate both functions into a single platform layer.

Smart Order Routers are the decision-makers in the chain. SOR systems factor in venue fees, latency, liquidity depth, and price improvement opportunities simultaneously to optimize execution outcomes. A well-configured SOR can route your order to a venue offering a better price than the one your broker defaults to, which is a direct benefit to your fill quality.

Key technology factors that affect execution speed and reliability:

- Message volume spikes. During high-activity periods, order queues at exchanges and ECNs grow rapidly. Message volume spikes and complex orders increase latency unpredictably, even on well-built infrastructure.

- Order complexity. Conditional orders with multiple parameters require more processing time than simple market orders.

- Co-location. Institutional traders place their servers physically close to exchange matching engines to reduce routing latency to microseconds. Retail traders rely on their broker’s infrastructure quality instead.

- ECN vs. market maker routing. ECNs match orders directly between participants, offering transparent pricing. Market maker routing may offer price improvement but introduces a principal conflict.

“Many retail traders mistake market-driven price volatility for execution failure. Execution systems simply process orders. The final price depends on supply and demand at the exact moment the order arrives at the venue.” The Technology Path of a Trade, Lime

Understanding the technology behind your broker matters because understanding execution mechanisms and order routing choices is the only way retail traders can grasp their true transaction costs and optimize strategies accordingly. For a detailed breakdown of how institutional order flow differs from retail routing, the analysis at institutional order flow is worth reading before you size up your positions.

重要なポイント

Order execution is the complete technological and regulatory process that converts your trading decision into a confirmed market position, and every stage from routing to matching affects your final fill price.

| ポイント | 詳細 |

|---|---|

| Execution vs. settlement | Execution happens in milliseconds; U.S. equity settlement completes one business day later under the T+1 cycle. |

| Order type selection | Market orders guarantee fills but not price; limit orders protect price but risk no fill in fast markets. |

| Slippage is dynamic | Slippage depends on volatility, order size, and liquidity depth, not broker error or platform failure. |

| Technology determines quality | OMS, EMS, and Smart Order Routers shape every fill; your broker’s infrastructure is as important as your strategy. |

| Price improvement exists | Wholesale market makers can fill retail orders above NBBO, but this benefit is not guaranteed on every trade. |

Why execution mechanics deserve more attention than most traders give them

Most traders spend the majority of their time on strategy and almost none on understanding how their orders actually get filled. That imbalance is a mistake, and I have seen it cost traders real money in ways they never traced back to execution.

The most common error is treating a bad fill as a platform glitch. In reality, the execution system worked exactly as designed. The market moved between submission and fill. That is slippage, and it is a cost you can manage with the right order type and the right broker infrastructure, but only if you understand what caused it.

Selecting a broker based on advertised spreads alone ignores the routing layer entirely. A broker with a 0.1 pip spread but slow SOR and no price improvement policy can cost you more per trade than one with a 0.3 pip spread and genuine best-execution routing. Request execution quality reports. If a broker cannot produce them, that tells you something important.

The traders I have seen execute most consistently do three things. They match their order type to market conditions rather than defaulting to market orders. They monitor their average slippage per instrument over time, not just per trade. And they treat execution as a recurring cost to be managed, not a fixed fee to be ignored. Perfection in execution is not achievable. Consistency and informed choices are.

— FX

Trade smarter with Ollatrade’s execution infrastructure

Ollatrade is built for traders who take execution seriously. The platform delivers fast, reliable order processing across forex, CFDs on metals, indices, stocks, energies, and cryptocurrencies, with infrastructure designed to minimize latency and maximize fill quality on every trade.

オラトレードの 外国為替取引プラットフォーム supports multiple order types, real-time execution monitoring, and MetaTrader 4 integration with expert advisors for automated strategies. Tight spreads and transparent routing mean you see your true transaction costs, not a number that looks good on a marketing page. Whether you are placing your first trade or managing a professional portfolio, Ollatrade gives you the tools and the execution quality to trade with confidence. Open your account today and put your strategy to work.

よくある質問

What is order execution in simple terms?

Order execution is the process by which a broker receives your buy or sell order, routes it to a market venue, and completes the trade at a confirmed price. The entire sequence from submission to fill typically takes milliseconds in modern electronic markets.

How does order execution differ from settlement?

Execution is the moment your order is matched and filled at a price. Settlement is the legal transfer of assets and cash, which under the U.S. T+1 cycle completes one business day after the trade date.

What causes slippage during order execution?

Slippage occurs when your actual fill price differs from your expected price, most commonly during high volatility, low liquidity, or when a large order consumes multiple levels of the order book at progressively worse prices.

What is the role of a Smart Order Router in execution?

A Smart Order Router analyzes multiple execution venues in real time, comparing liquidity, fees, and price improvement opportunities to select the optimal path for your order, directly affecting fill quality and cost.

Which order type gives the best execution quality?

There is no single best order type. Market orders guarantee fills but not price. Limit orders protect price but risk no fill. The best choice depends on your instrument’s liquidity, current market volatility, and whether speed or price control matters more for that specific trade.